LDTI is the most significant change in decades to the existing accounting requirements under US Generally Accepted Accounting Principles (USGAAP) for long duration contracts that are non-cancellable or guaranteed renewable contracts such as life insurance, disability income, long-term care, and annuities.

The ultimate objectives of this accounting standard change are to:

- Provide a standardized framework allowing for a better comparison of risk across insurers

- Improve the financial reporting of long-duration insurance contracts through improved information regarding the amount, timing and uncertainty of cash flows

- Aid investors with improved information and disclosures which help to better understand the financial performance and risk of an insurance company

For SEC filers, LDTI is effective for fiscal years beginning after December 15, 2023. For non-SEC filers it is effective two years later, on December 15, 2025. BDO is helping insurers navigate the complexities of LDTI adoption. We have experienced technology, accounting, and actuarial practices to efficiently progress through the LDTI journey, leveraging a series of accelerators we have established specifically focused on the adoption of new regulatory standards. This article is focused on the data and technology considerations for the LDTI journey.

Why LDTI matters in the world of Data

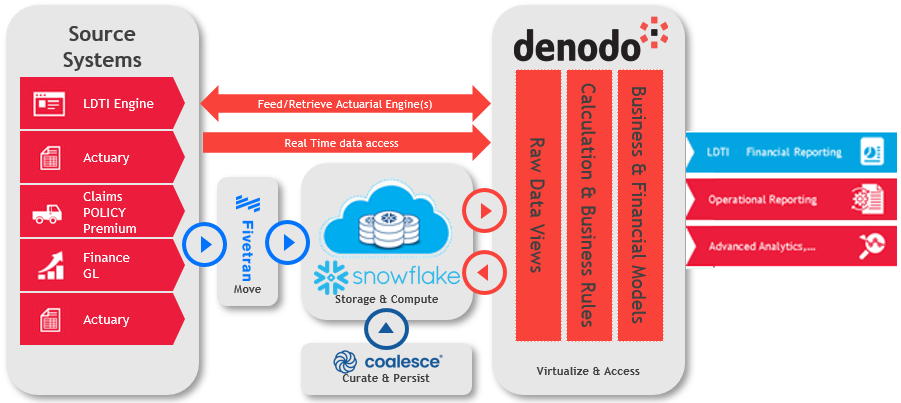

The introduction of the LTDI standard is often a catalyst for Life Insurers in the adoption of modern data management practices. Compliance can’t be achieved without substantial alignment of supporting IT systems to match new accounting policies, data accessibility and data analytics/reporting requirements. For many insurers, this is the time to question the investment in upgrading legacy point-to-point systems using LDTI as the catalyst to upgrade to a logical data fabric that captures all components of the requirement—allowing for alignment of the data flows for the end-to-end process.

Here are a few of the key implementation realities that insurers are faced with as they look to decide on upgrading their point-to-point system or upgrade to a new Logical Data Fabric environment:

- The complexity of data integration for most LDTI implementations is high given the significant footprint of policy, claims, financial, investments, and reinsurance data usually residing in a variety of source systems.

- The approach to data integration is a key consideration for the IT department because of its broader impact across the technology and data landscape. Those who combine the integration needs of LDTI with the integration needs of other business objectives can achieve economies of scale in doing them together, leveraging the same integration strategy and platform.

- LDTI presents a catalyst opportunity for IT to move away from a legacy point-to-point approach and adopt a modern data fabric approach. This facilitates the data connectivity for LDTI and sets the foundation for data maturity advancement, enabling advance analytics outcomes that leverage the potential of artificial intelligence.

- When looking at the total cost of ownership, agility, maintainability, advancing data maturity, advancing analytics, and being cloud ready, there is a clear advantage for a data hub strategy versus a point-to-point strategy.

- Given the rich dataset required for LDTI, it’s a great opportunity to look at your enterprise integration strategy and progressively modernize it through the LDTI initiative.

While many insurers may challenge the cost/benefit of transitioning to newer data fabric as they seek to comply with the new standard, our experience is that building on a point-to-point strategy is more expensive than implementing a new data fabric platform. Such upgrades also do not easily position the insurer to advance their overall data maturity/governance and to set the stage for capitalizing on the potential of advanced analytics.

The opportunity

The deadline for LDTI compliance is rapidly approaching, making it crucial for insurers to examine and act on their compliance plans sooner rather than later. The question for most insurers now is: will they simply create a minimum viable solution or will they seize this opportunity to truly transform their business and take a market leadership position?

At BDO, we have established deep expertise in building solutions that immediately solve these regulation requirements while laying the foundation for solid enterprise data management practices.

The InsurMesh LDTI Accelerator

Early adopter insurers of LDTI have realized that the maturity of the data platform is directly related to the complexity of LDTI adoption. Insurers with low maturity data platforms generally have a harder time with LDTI adoption. As a result, we have established a data platform accelerator known as InsurMesh that quickly advances the data maturity of an Insurer and eases the burned of LDTI adoption.

The InsurMesh accelerator is based on the Denodo Platform. It not only accelerates the path to LDTI compliance, but also advances an insurers data maturity for advanced analytics.

The InsurMesh accelerator shortens the timeline of LDTI implementations with pre-packaged data connectivity, workflow processing, a calculation library, and reports aligned with the requirements of LDTI. It contains fundamental best practices to be the gold standard for pragmatic data governance and operations. The InsurMesh accelerator generally shortens the implementation time by up to 50% through our library of pre-packaged LDTI modules. The same pre-packaged modules set the foundation for advanced analytics, addressing a broad range of customer, market strategy, operations, finance, risk, loss, and performance analytics scenarios.

We would be pleased to connect with you to showcase the acceleration InsurMesh can provide in the LDTI journey.

- Achieving LDTI Compliance using Data Virtualization - March 10, 2022